Do you know what a production possibility curve is and how it can help you make better business decisions? If not, this guide is for you! In this article, we will be discussing the production possibility curve in detail, with an example to illustrate everything. So, stay tuned!

What are the three types of production possibility curve?

A production possibility curve (PPC) is a graphical representation of the relationship between the cost of producing a good or service and the quantity produced. It can be used to evaluate the profitability of different strategies for producing a particular good or service.

There are three types of PPCs:

The AC curve shows how much additional income can be earned by increasing output above the current level. The slope of the AC curve indicates the relative price sensitivity of output.

The BC curve shows how much additional costs can be incurred by increasing output above the current level. The slope of the BC curve indicates the relative cost sensitivity of output.

The MR curve shows how much additional revenue can be generated by increasing output above the current level. The slope of the MR curve indicates the relative price elasticity of demand for output.

What is the production possibility curve?

The production possibility curve is a graphical representation of how much output an economy can produce with various amounts of inputs. The curve helps policymakers make choices about which economic activities to promote and which to discourage.

The production possibility curve is shaped like a J-curve, with the horizontal axis representing the amount of input (measured in units of output) and the vertical axis representing the amount of output (measured in units of input). Each point on the curve represents a particular production combination that can be produced using available resources.

Policymakers use the production possibility curve to understand how much economic activity is possible given certain constraints. For example, if you are trying to decide how much oil to drill in a particular field, you might look at the production possibility curve to see how many wells you can drill with different levels of input.

The shape of the production possibility curve reflects important economic dynamics. For example, when there are more resources available, the curve slopes down towards the right because more output can be produced with each additional unit of input. Conversely, when there are fewer resources available, the slope of the curve will be higher because more output can be produced with each additional unit of input.

What is production possibility curve with example?

A production possibility curve is a graphical representation of the trade-offs between different inputs in a production process. It can help managers make informed decisions about what to produce and how much to produce.

The production possibility curve shows the quantity of a good that can be produced at various price levels. At a given price, the quantity of the good produced increases as the amount of one input (x-axis) increases, but decreases as the amount of another input (y-axis) increases. The point on the curve corresponding to this price is called the “production possibility frontier.”

When producers have multiple choices for inputs, they can use a production possibility curve to find the optimum combination of inputs that produces the greatest quantity at the lowest cost. For example, suppose you are producing widgets and you can use two types of plastic: hard plastic and soft plastic. You could place your business on a production possibility curve by plotting how much each type of plastic costs against how many widgets each type can produce.

If you are producing widgets for sale in a store, you would want to place your business on the production possibility frontier so that you maximize your profits.

What are the 4 assumptions of a production possibilities curve?

If you are in business, you have probably heard of the production possibilities curve (PPC). The PPC is a graph that shows how much output a company can produce at different prices.

In this article, we will explain what the four assumptions of the PPC are and how they help businesses make decisions.

The four assumptions of the PPC are:

1. There is a fixed quantity of resources that can be used to produce a good or service.

2. The cost of each unit of output remains constant over time.

3. The technology used to produce a good or service changes over time but the total quantity of resources used to produce a good or service does not change.

4. There is an inverse relationship between price and quantity produced. That is, as price goes up, quantity produced goes down, and as price goes down, quantity produced goes up.

What are the characteristics of PPF?

The production possibility frontier (PPF) is a graphical representation of the relationship between a given quantity of output and the number of inputs used to produce that output. It can be used to explore all possible combinations of inputs and outputs, from which the most efficient combination can be selected.

The PPF typically has a U-shape, with peaks representing the highest possible output levels achievable with a certain number of resources, and valleys representing the lowest possible output levels. The middle zone represents an equilibrium point where the amount of output produced is at its maximum.

There are many factors that can influence a business’s decision-making process, so it’s important to understand how the PPF can help you make optimal decisions. For instance, if you’re looking to expand your business into new markets or increase production on existing products, using the PPF can help you identify which areas are most promising.

What is the importance of the PPC in economics?

The Production Possibility Curve (PPC) is one of the most important tools in economics. It is used to help economists understand how much different items can be produced at different prices.

The PPC shows how much a specific good or service can be produced at different prices. The curve starts at the point where it is impossible to produce any more of the good, and continues to grow as prices go up.

The PPC is important because it helps economists understand how efficient businesses are. If a business can produce more of a good than another business, the first business will be able to sell more of the good at a higher price. This will make the first business very profitable, and likely lead to the second business closing down.

What is the shape of PPC curve?

The production possibility curve ( PPC ) is a graphical representation of the efficient use of resources for a company or individual. The PPC graph displays the possible output of a company, at different levels of input, by plotting the amount of each resource used against the quantity of output produced.

The shape or form of the PPC curve can be determined by how much each input resource costs and how much output can be produced with those inputs. The most common PPC shapes are linear (straight line), inverted-U, and S-shaped.

Linear: When all inputs are relatively equal, a linear PPC curve will result in an equally distributed amount of output at each level of input. For example, if a company has 10 workers and can produce 20 widgets per day with five different types of raw materials, their PPC curve will look like this:

Inverted-U: When one input costs more than another, the extra cost will show up as an increase in the quantity required to produce the same amount of output on the PPC curve. For example, if a company has five workers and can produce 20 widgets per day with three different types of raw materials, their PPC curve will look like this:

What is the slope of PPC?

A production possibility curve (PPC) is a graphical representation of the relationship between the costs of producing different quantities of a good or service. The PPC can be used to evaluate the profitability of various production strategies.

The slope of the PPC represents the increase in profitability with increased output. The steeper the slope, the more profitable it is to produce more goods or services. In most cases, the slope is determined by two factors: input costs and output prices.

Input costs include everything that goes into producing a good or service, such as wages, raw materials, and equipment rentals. Output prices include all costs associated with selling a good or service, such as shipping and marketing expenses.

To create a PPC, start by drawing a simple graph showing how total costs (in dollars) change with output (in units). Then determine the slope of this graph by dividing cost by output. The steeper the slope, the more profitable it is to produce more goods or services.

What do you mean by production possibilities of an economy?

A production possibility curve (PPC) is a graph that displays the number of outputs an economy can produce at different combinations of inputs. The PPC shows the maximum amount of output that can be achieved with the available resources, given certain constraints on either the quantity or quality of inputs.

The PPC is often used to analyze how an economy might be able to growth or shrink its production. When graphed, the PPC will typically have a shape that resembles a U-shaped curve. The U-shape reflects two key factors – potential output and constraint. Potential output is the maximum amount of output an economy could produce if all inputs were available at their full potential. Constraint refers to any limitations on how much input an economy can use, including things like physical limits on inputs or legal restrictions on output.

The slope of the PPC tells us how much broader or narrower the curve is in relation to its horizontal axis. The steeper the slope, the more constrained (or restricted) the resources are in terms of potential output. The shape of the PPC also reflects how Likely different combinations of resources are to be used to achieve a specific level of output.

The following figure is an example of a production

Why does PPC expand outwards?

The production possibility curve is a graphical tool used in economics to illustrate the relationship between different resources and the amount of goods that can be produced. It is commonly used when evaluating investment opportunities. The production possibility curve shows the amount of output that can be produced with a given combination of inputs, or resources.

The horizontal axis represents inputs (labor, capital, etc.), while the vertical axis represents output (sales, profits, etc.). As you can see in the diagram above, as more resources are available (i.e. more employees or more capital), the amount of output that can be produced increases until there is a point of saturation. Beyond that point, adding more resources will not result in any further increase in output.

This is why PPC expands outwards: because beyond a certain point, increasing the number of ads or keywords does not result in an increase in conversion rates. In other words, it’s no longer worth your time and money to spend more on ads since there’s not going to be a corresponding increase in revenue.

While this might seem like bad news at first, it actually presents an opportunity: because PPC campaigns tend to be expensive, by finding campaigns that are no longer profitable you

How does the production possibilities curve describe economic growth?

A production possibilities curve (PPF) plots the possible quantity of a good or service that can be produced given a certain income level. The shape of the curve reflects the economy’s ability to produce goods and services at various price levels.

The production possibilities curve typically starts at the bottom left-hand corner and slopes downward as more and more resources become available. When the curve reaches the right-hand end, there are no more additional supplies of the good or service that can be produced at a lower price. This is because at that point, all potential producers have already engaged in production and any new production would only result in replacing existing goods and services with ones of lower quality.

The slope of the PPF tells us how much more potential output exists when prices are raised from one level to another. For example, if the PPF slopes downwards from left to right, this means that when the price for a good rises, producers can produce an increasing amount of that good before running out of supplies. If the PPF slopes upwards from left to right, this means that when prices rise, producers can only produce a limited amount of the good before running out of resources.

What causes the production possibilities curve to shift outward?

When a company expands its production capabilities, it faces a new constraint on its potential output. The more productive resources the company can bring online, the higher is the possibility of exceeding current sales levels.

But there’s still another factor at play: when demand for a good increases, companies are forced to lower their prices in order to retain market share. This process creates opportunities for new competitors who enter the market with lower prices, forcing the original company to either raise its prices or lose market share entirely.

This competition leads to two outcomes: either the original company can successfully expand its market share by offering consumers more value for their money, or it will fall victim to price erosion and eventually go out of business.

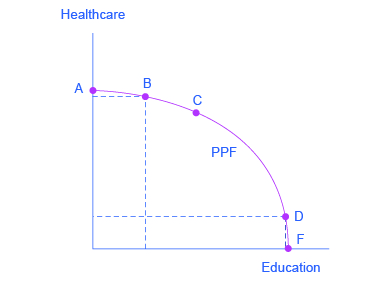

The diagram below illustrates these concepts with an example. At point A, the production possibilities curve shows how much product can be produced with existing resources. As more resources are brought online, the curve shifts outward, indicating that more product can be produced at each price point. However, as demand for the product increases, companies must take measures to maintain their marketshare (points B and C). This means lowering prices in order to attract buyers and stay afloat in a saturated market.

Eventually (point D), companies will

production possibility curve notes

A production possibility curve is a graphical tool used to illustrate the opportunity for producing a good or service in an economy. The graphic shows the amount of output that can be produced at different cost levels (usually expressed asLabor Hours) under various market conditions.

The graphic provides an overview of the cost of producing a good or service, and highlights the range of potential output at different prices. It can be helpful in making decisions about investments and pricing strategies.

The following are some key points to keep in mind when interpreting a production possibility curve:

1. The height of the curve reflects the amount of output that can be produced with given amounts of labor and resources.

2. The bottom of the curve reflects the point where production costs are equal to total revenue. At this point, producers are able to earn a profit by selling their product.

3. The slope of the curve indicates how much easier or harder it is to produce additional units of output at various costs. Slope is generally determined by comparative costs: the higher the cost, the steeper the slope.

production possibility curve pdf

Production possibility curve is a graphical representation of the possible output from a production process under different conditions. The figure helps to identify the point where increased input will result in more output, and vice versa.

The Production Possibility Curve is most commonly used in business to help managers make decisions about how to allocate resources and what levels of output they are able to achieve. It is also used in economics to illustrate how different inputs (labour, materials, machines) lead to different outputs (goods and services).

There are many ways to produce one good. Suppose I can produce two goods, A and B. If I can produce either good at any given quantity, then the production possibility curve for both goods would be a vertical line. If I can only produce one good at any given quantity, then the production possibility curve for that good would be a horizontal line.

Now suppose that I can produce both goods at the same time but only if I have enough workers. If I increase the number of workers, then the production possibility curve shifts to the right so that more output can be produced with fewer workers. Similarly, if I decrease the number of workers, then the production possibility curve shifts to the left so that more output can

production possibilities curve worksheet

When you are considering how to Produce a good or service, what is the best way to do it? The answer lies on the production possibilities curve.

The production possibilities curve shows the various combinations of inputs that can be used to produce a good or service at different costs. It is represented by a graph with two axes: input (output) and cost. The horizontal axis represents output and the vertical axis represents cost. The area under the curve (AUC) shows how much output can be produced at a given cost. The shape of the curve reflects opportunities for producing more output with less input at a lower cost, and then opportunities for producing more output with more input at a higher cost.

To use the production possibilities curve, you first need to identify your industry and your target market. Then you need to figure out what type of product or service you want to produce. You also need to know your costs of producing each type of product or service. Finally, you need to identify where on the production possibilities curve your costs are lowest. This is where you should set your production goals.

The following example uses data from the hospitality industry to illustrate how the production possibilities curve works. Suppose Lisa wants to open her

what is production possibility curve explain with diagram

A production possibility curve (PPC) is a graphical representation of the various combinations of inputs that can be used to produce a good or service. It was first developed in the 18th century by the French economist Pierre-Simon Laplace.

The PPC is typically used to analyze the economics of production. In particular, it can be used to identify the point at which an increase in the input quantity or price will result in a change in output quantity or price.

To create a PPC, you need to first identify the following four quantities:

Output: The amount of output that can be produced using a given combination of inputs.

Input: The amount of each input that is used to produce output.

Utility: The amount of happiness that can be obtained from producing a given output.

Cost: The cost of producing output using a given combination of inputs.